How to correctly fill out the kudir for income taxation. How to fill out the kudir for an entrepreneur on income minus expenses. Payments with electronic money

Section 4 of the book of accounting for income and expenses is filled out by those organizations and entrepreneurs who pay the simplified tax system on income. This section reflects the amount of tax deduction by which the simplified tax system is reduced. Here you will find an example of filling out (item) section 4 in the Income and Expense Accounting Book.

Attention! The following will help you fill out section 4 KUDiR correctly:

Let us remind you that the single tax, when simplified, can be reduced by contributions for compulsory social insurance, voluntary personal insurance of employees and some other expenses. The fact is that organizations that are taxed under the simplified taxation system have the right to reduce the amount of the simplified tax system or advances for it by tax deduction. This deduction includes:

- insurance contributions for compulsory social insurance accrued in accordance with the Tax Code of the Russian Federation;

- contributions for voluntary personal insurance of employees in case of their illness

- the amount of temporary disability benefits paid from the organization’s funds. But only to the extent not covered by insurance payments, and under voluntary insurance contracts (if any were concluded by the organization).

Fill out KUDiR in the BukhSoft program. The program will generate a file with the document and check it. All you have to do is download and print the Book

Get a consultation ⟶

Section IV is intended for calculating tax deductions in the book of income and expenses. The rules for filling out this section are established in Section V of the Procedure, approved by Order of the Ministry of Finance dated October 22, 2012 No. 135n.

Calculate the deduction in section IV of the Accounting Book. But legislators did not really provide explanations on how to fill it out. Accountants figure it out themselves. Our tips will help you. Here you will find an example of filling out item 4 in the book of income and expenses.

Book of income and expenses: sample of filling out section 4

You record in Section IV all benefits issued and insurance premiums paid. The total under column 10 may exceed the 50 percent deduction limit. How can you explain to the tax authorities why you did not reduce the tax on all contributions and benefits recorded in section IV? Where to record the unused deduction so as not to lose this amount and include it in the tax calculation for the next period?

In Section IV of the Accounting Book there is no special column for contributions and benefits not included in the deduction. Therefore, reflect these amounts in another document. For example, in an accounting statement. Draw up such a certificate at the end of each quarter in which there is an unused deduction. It can be carried forward to the next reporting period.

It is convenient to work with documents in . It is suitable for organizations and individual entrepreneurs. The program will automatically generate and print all the necessary primary data. It also includes uploading transactions to 1C, automatic generation of any reporting, and much more.

One caveat. Contributions and benefits that exceed the limit and are not included in the deduction, you have the right to include in the tax calculation only in the current calendar year. Unused deductions cannot be carried over to the next year. After all, tax reduction is allowed only on contributions and benefits paid in the current tax period (clause 3.1 of Article 346.21 and clause 1 of Article 346.19 of the Tax Code of the Russian Federation). Here is an example of filling out the Income and Expense Book.

Example

Cosmos LLC applies the simplified tax system to the object of income. In September 2016, the accountant paid the employee benefits for 5 days of illness. The accrued amount is 2500 rubles, including at the expense of Cosmos LLC - 1500 rubles. The employee received an allowance minus personal income tax of 2,175 rubles. (2500 rub. - 2500 rub. X 13%). We will show how the accountant will reflect the paid benefits in section IV of the Accounting Book.In column 3, the accountant will indicate the month for which he accrued the benefit. And in column 8, the amount of the benefit is at the expense of the company, without deducting personal income tax (see fragment of section IV below).

Sample of filling out KUDiR

Section 4 KUDiR: benefits from own funds

You pay sick leave benefits to employees from two sources: Social Insurance Fund and the company’s own funds. It is unclear how much of the benefits paid can be recorded in Section IV of the Account Book. And is it necessary to reduce benefits by the amount of personal income tax withheld?

In column 8 of section IV of the Accounting Book, write down only benefits issued at the expense of your company (subclause 2, clause 3.1, article 346.21 of the Tax Code of the Russian Federation). That is, amounts due for the first three days of illness or injury of the employee himself (Clause 1, Part 2, Article 3 of Federal Law No. 255-FZ of December 29, 2016). At the same time, include in the deduction under the simplified tax system all accrued benefits, including personal income tax (letter of the Ministry of Finance of Russia dated April 11, 2013 No. 03-11-06/2/12039). But the part of the benefit that is accrued at the expense of the Social Insurance Fund does not need to be entered in column 8.

Section 4 KUDIR: amounts as they are paid

Employers have the right to reduce tax under the simplified tax system by no more than 50% (clause 3.1 of article 346.21 of the Tax Code of the Russian Federation). Therefore, you will not include all contributions and benefits in the deduction, but within this limit. And you need to figure out whether to record excess amounts in Section IV.

Do what is most convenient for you. You can record all contributions and benefits in Section IV. Or only those that you include in the deduction. This issue is not resolved in the Procedure for filling out the Accounting Book (Appendix No. 2 to Order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n). Therefore, do at your own discretion. Write down the chosen method in your internal document. For example, in tax accounting policies. When checking, tax authorities may ask on what basis you are filling out Section IV. It would be better if the answer to this question is straightforward.

If you choose to record all contributions and benefits, complete Section IV as amounts are paid. And with the second option, you fill out section IV only after the reporting period has ended. And you know the amount equal to 50% of the tax. Only within its limits do you generate a deduction.

Example of filling out KUDiR

An example will show you how to fill out a book of income and expenses when using a simplified taxation system.

Example

Almaz LLC applies the simplified tax system with the object “income”. The tax rate is 6%. The taxable income of the organization for 9 months of 2016 amounted to RUB 5,240,000. Section IV of the Accounting Book for 9 months of 2016 reflects contributions and benefits equal to 184,000 rubles. For the first quarter, the advance payment under the simplified tax system amounted to 48,000 rubles. At the end of the six months, the amount to be paid additionally is RUB 52,000. We will show how the accountant of Almaz LLC will determine the amount payable for 9 months of 2016.First, the accountant of Almaz LLC will calculate the amount of the advance payment for 9 months. It is equal to 314,400 rubles. (RUB 5,240,000 × 6%). Next, he will calculate the maximum amount by which the tax can be reduced. 50% of the accrued tax will be 157,200 rubles. (RUB 314,400 × 50%). This is less than the amount of contributions and benefits reflected in Section IV of the Account Book. This means that Almaz LLC has the right to reduce the tax by only 157,200 rubles. And the company must transfer the amount minus payments for the first quarter and half of the year no later than October 25, 2016. The advance payment for the additional payment for 9 months of 2016 is equal to 57,200 rubles. (RUB 314,400 - RUB 157,200 - RUB 48,000 - RUB 52,000).

Who runs KUDIR?

| Tax regime | Entrepreneurs | Organizations |

|---|---|---|

| Lead / Don't lead | ||

| simplified tax system | ||

| BASIC | They always do it and calculate the tax on its basis | |

| PSN(Patent) | They do, but not for calculating taxes. The goal is to know that the amount of income does not exceed 60 million. | This tax regime cannot be applied |

| UTII | They don’t lead, because the tax does not depend on income. Still, sometimes they require it from the tax office (by law they should not), especially if separate accounting of different regimes is used. Then you can keep it in a simplified form. | |

| Unified agricultural tax | They always do it and calculate the tax on its basis. | They don’t lead, because do accounting. |

How to lead? By hand or electronically on a computer?

You can keep a book either by hand on paper or electronically. Moreover, you can change the order of keeping a book even in the middle of the year.

For every new year you need to start a new book.

What to reflect?

| Operation | Reflect? |

|---|---|

| Reflect/Do not reflect | |

| Taxable income | Always reflect |

| Insurance premiums for individual entrepreneurs | |

| Insurance premiums for employees | Reflect if they reduce the amount of tax. It is not reflected on PSN. |

| Topping up your own current account | They don't reflect. Because This is not income and does not affect tax. |

| Expenses | . . |

| Transfer money to your account | |

| Payroll issuance | Reflected on the simplified tax system "Income-Expenditures" and OSNO. They do not reflect on the PSN and the simplified tax system “Income”. |

| Interest-free loan from the founder | |

| Dividend payment | They don't reflect. Because This is not income or expense and does not affect tax. |

| Payment of tax simplified tax system | They don't reflect. Because This is not an expense and does not affect tax. |

| Payment of personal income tax (OSNO) | They don't reflect. Because This is not an expense and does not affect tax. |

| Payment of personal income tax (for employees) | They don't reflect. Because this tax does not belong to the organization at all. The organization acts as an agent. |

| Acquisition of KKM | Can be taken into account and reflected in expenses. |

| Product purchased including VAT | VAT is taken into account and reflected in expenses in proportion to the cost of goods sold. |

| Penalties and fines | They don't reflect. Because This is not an expense and does not affect tax. |

| Refund of overpaid amount | Reflected in income with a minus sign at the beginning. |

Reflect all indicators in KUDIR rounded in rubles, without kopecks.

How to submit?

Is it necessary to submit KUDiR to the Federal Tax Service?

The book is submitted to the Federal Tax Service only if the Federal Tax Service itself requests it. The book must be bound and numbered in any case.

Until 2013, KUDIR could be voluntarily submitted and certified. They don't do this now.

How to flash a book?

The book must be laced, the pages numbered and on the back of the last page a sticker (of arbitrary size, about 3*4 cm) should be pasted - “so many sheets laced and numbered” and your signature.

Fines

When checking, if the book is not there, then a fine of 10,000 to 30,000 rubles (Article 120 of the Tax Code since 2015) for individual entrepreneurs and organizations. There may also be a 200 ruble fine for the official (manager or individual entrepreneur). This will also be a reason for further verification.

Shelf life

Because The book is needed to draw up and substantiate the declaration, so it should be kept for 4 years. Taxpayers can carry forward losses from previous years or submit an adjustment for any period, so it is advisable to keep it for 11 years.

simplified tax system

Form

From January 1, 2018, a new KUDiR (order of the Ministry of Finance of Russia dated December 7, 2016 No. 227n.). The ability to reflect the trading fee has been added to it.

If there are not enough sheets or lines in the book, then another book is filled.

Zero KUDiR

How to fill?

Even with a zero simplified tax system, an individual entrepreneur (or organization) must have a zero ledger for accounting income and expenses: Zero CD&R - sample (for reporting 2018-2019).

A zero declaration of the simplified tax system and KUDIR can be generated for free and sent via the Internet from (You need Tariff Zero).

Example of filling out the simplified tax system for income (6%)

Sections II and III under the simplified tax system “income” are always left blank.

How to fill?

Receipts on account, write the date of receipt of income and the number of the payment order (p/n) from the bank. The bank issues a payment order to you after receipts are received into the account. Example: 01/25/2018 p/p No. 503

Cash receipts, write the date of receipt of income and the Z-report number. Example:

Penalties and fines, in KUDIR or in the simplified taxation system declaration are not displayed anywhere.

Return: you sold something (provided a service), you were paid more and then you returned the overpaid amount to the buyer. Then you need to enter the initial amount in full, and then reduce the “Income” column, i.e. reflect (as of the date of return) in the Income column the amount of the return with a minus.

Refund of overpaid amount: services for December 2018 under contract PR-1356-10/18

When simplified, the cash method of accounting for income is used, in which income is entered by the date of receipt of money, and not the date of conclusion of the contract.

Income received: Payment for services for December 2018 under contract PR-1356-10/18 or Receipt at the cash desk: revenue from cash registers for 04/29/2018 Z-report No. 00000001. The content of the income transaction is not so important for the tax authorities; due to errors and inaccuracies, your taxable income will certainly not be reduced.

Replenishment of an individual entrepreneur's own account is not displayed in the book. For organizations: an interest-free loan and an increase in the authorized capital are also not considered income and are not shown in the ledger.

If BSO is applied?

Since 2013, a new section IV has been filled in, “Expenses provided for in paragraph 3.1 of Article 346.21 of the Tax Code of the Russian Federation, which reduce the amount of tax paid (advance tax payments). It is filled out only for the simplified tax system Income. Please note that not all insurance contributions are indicated in this section, but only those that reduce the simplified tax. In Table 4, in column 3 "The period for which the payment of insurance premiums was made, payment of temporary disability benefits provided for in columns 4 - 9" indicate "2013" or "January 2013".

Reflection of Pension Fund contributions

Section IV is filled out only by those who have income on the simplified tax system.

Reflected in IV. Expenses provided for in paragraph 3.1 of Article 346.21 of the Tax Code. They are only reflected if they reduce tax. Those. If the tax is 0 rubles, then you don’t need to enter anything there. If the tax is 500 rubles, then you can enter no more than 500 rubles. Fees must be paid. The reduction of the simplified tax system is voluntary. If for some reason you don’t want to (for example, you didn’t enter 10 rubles there, you don’t want to correct it) or you can’t reduce the simplified tax system, then you don’t have to fill out this section.

Reflection of trade fee

On January 1, 2018, a new KUDiR appeared (order of the Ministry of Finance of Russia dated December 7, 2016 No. 227n.). The ability to reflect the trading fee has been added to it.

Section V “The amount of the trade fee that reduces the amount of tax paid in connection with the application of the simplified taxation system (advance tax payments) calculated for the object of taxation from the type of business activity in respect of which the trade fee is established for the reporting (tax) period” is filled out only those who have income on the simplified tax system

By analogy with Section IV, only the trade fee that reduces the tax of the simplified tax system is displayed here, and not the entire paid trade fee (although it may be all).

An example of filling out the simplified tax system “income minus expenses”

With the simplified tax system income-expenses, the book must be treated with great attention. For tax authorities, expense items, their justification and confirmation are very important (sometimes they even require photographs from events).

Assets worth more than 40,000 rubles are classified as fixed assets.

How to fill?

Read above about how to fill out “Income”.

Sections IV and V under the simplified tax system “income-expenses” are always left blank.

Date and number of the primary document

Item for resale Example: 02/28/2010 Consignment note No. 1092

Although the Ministry of Finance believes that the name of the product may be in a foreign language (Letter of the Ministry of Finance of the Russian Federation dated May 18, 2017 No. 03-01-15/30422) it is better to translate into Russian (Letter of the Federal Tax Service dated December 10, 2004 No. 03-1-08/2472/16) .

Services, write the date of expenditure for the service and the Z-report number. Example: 04/29/2018 Check Z-report No. 00000001

Expenses made in cash, write the date of receipt of the sales receipt and its number. Example: 05/29/2018 Check No. 00000001

Return: you sold something (provided a service), you were paid more and then you returned the overpaid amount to the buyer. Then you need to reduce the “Income” column, i.e. reflect (as of the date of return) in the Income column the amount of the return with a minus.

Expenses for the purchase of goods are included after its sale.

“Section III” Calculation of the amount of loss that reduces the tax base for the tax paid in connection with the application of the simplified taxation system is filled out if there were losses in the past or in the current period. can be carried over to the next period.

Reflection of Pension Fund contributions

You can display the amounts of the Pension Fund, benefits at the expense of the employer, etc. as part of expenses - reducing the tax base. Again, reducing this base is the right, but not the obligation of the taxpayer. If you forget to enter something and do not reduce the simplified tax system base, this will not be a violation.

Instructions

COMPLETING THE BOOK OF ACCOUNTING INCOME AND EXPENSES OF ORGANIZATIONS

AND INDIVIDUAL ENTREPRENEURS USING

SIMPLIFIED TAX SYSTEM

List of changing documents

I. General requirements

1.1. Organizations and individual entrepreneurs applying the simplified taxation system (hereinafter referred to as taxpayers) maintain a Book of accounting of income and expenses of organizations and individual entrepreneurs applying a simplified taxation system (hereinafter referred to as the Book of accounting of income and expenses), in which, in chronological order, based on primary documents, positional way to reflect all business transactions for the reporting (tax) period.

1.2. Taxpayers must ensure the completeness, continuity and reliability of recording the indicators of their activities necessary for calculating the tax base and the amount of tax.

1.3. The Book of Income and Expenses is maintained in Russian. Primary

language or languages of the peoples of the Russian Federation, must have a line-by-line translation into Russian.

1.4. The book of income and expenses can be kept both on paper and in electronic form. When maintaining the Book of Income and Expenses in electronic form, taxpayers are required to print it out on paper at the end of the reporting (tax) period. For each tax period, a new Book of Income and Expenses is opened.

1.5. The book of income and expenses must be laced and numbered. On the last page of the Income and Expense Book, numbered and laced by the taxpayer, the number of pages it contains is indicated, which is confirmed by the signature of the head of the organization (individual entrepreneur) and sealed with the seal of the organization (individual entrepreneur) (if there is a seal). On the last page of the taxpayer’s numbered and laced Income and Expense Book, which was kept electronically and printed on paper at the end of the tax period, the number of pages it contains is indicated, which is confirmed by the signature of the head of the organization (individual entrepreneur) and sealed with the seal of the organization (individual entrepreneur). entrepreneur) (if there is a seal).

(as amended by Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n)

1.6. Correction of errors in the Income and Expense Accounting Book must be justified and confirmed by the signature of the head of the organization (individual entrepreneur) indicating the date of correction and the seal of the organization (individual entrepreneur) (if there is a seal).

(as amended by Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n)

II. Procedure for filling out Section I "Income and Expenses"

ConsultantPlus: note.

Federal Law dated 04/06/2015 N 84-FZ amended paragraph 1 of Article 346.15 of the Tax Code of the Russian Federation from January 1, 2016, according to which, when determining the object of taxation, income determined in the manner established by paragraphs 1 and 2 of Article 248 of the Tax Code of the Russian Federation is taken into account.

2.4. Column 4, in accordance with paragraph 1 of Article 346.15 of the Tax Code of the Russian Federation (hereinafter referred to as the Code), reflects income determined in the manner established by paragraphs 1 and 2 of Article 248 of the Code.

(as amended by Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n)

Column 4 does not take into account:

income of an organization subject to corporate income tax at the tax rates provided for in paragraphs 1.6, 3 and 4 of Article 284 of the Code, in the manner established by Chapter 25 of the Code;

(as amended by Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n)

ConsultantPlus: note.

Federal Law dated November 24, 2014 N 366-FZ, paragraph 4 of Article 224 of the Tax Code of the Russian Federation was declared invalid as of January 1, 2015.

income of an individual entrepreneur, subject to personal income tax at the tax rates provided for in paragraphs 2, 4 and 5 of Article 224 of the Code, in the manner established by Chapter 23 of the Code.

In accordance with subparagraph 1 of paragraph 1 of Article 346.25 of the Code, organizations that, before the transition to the simplified taxation system when calculating corporate income tax, used the accrual method, when transitioning to the simplified taxation system in column 4 on the date of transition to the simplified taxation system, reflect in their income amounts of money funds received before the transition to a simplified taxation system in payment for contracts, the execution of which the taxpayer carries out after the transition to a simplified taxation system.

In accordance with subparagraph 3 of paragraph 1 of Article 346.25 of the Code, funds received after the transition to a simplified tax system are not included in the tax base if, according to the rules of tax accounting on an accrual basis, these amounts were included in income when calculating the tax base for corporate income tax.

2.5. In column 5, the taxpayer reflects the expenses specified in paragraph 1 of Article 346.16 of the Code. The procedure for recognizing and accounting for expenses when determining the tax base for tax paid in connection with the application of the simplified taxation system is established by paragraphs 2 - 4 of Article 346.16, paragraphs 2 - 5 of Article 346.17, paragraphs 2, 3, 5, 7 and 8 of Article 346.18 and paragraphs 1, 2.1, 4 and 6 of Section 346.25 of the Code.

Column 5 must be completed by a taxpayer applying a simplified taxation system with the object of taxation in the form of income reduced by the amount of expenses.

A taxpayer applying a simplified taxation system with the object of taxation in the form of income, in column 5 reflects:

actually incurred expenses provided for by the conditions for receiving payments to promote self-employment of unemployed citizens and stimulate the creation by unemployed citizens who have opened their own businesses of additional jobs for the employment of unemployed citizens at the expense of the budgets of the budgetary system of the Russian Federation in accordance with programs approved by the relevant government bodies;

actual expenses incurred from financial support in the form of subsidies received in accordance with the Federal Law of July 24, 2007 N 209-FZ “On the development of small and medium-sized businesses in the Russian Federation” (Collected Legislation of the Russian Federation, 2007, N 31, Article 4006).

A taxpayer applying a simplified taxation system with the object of taxation in the form of income also has the right, at his discretion, to reflect in column 5 other expenses associated with the receipt of income, taxation of which is carried out in accordance with the simplified taxation system.

Help for Section I

2.6. The reference part of Section I is filled out by the taxpayer who has chosen “income reduced by the amount of expenses” as the object of taxation.

2.7. Line code 010 indicates the amount of income received by the taxpayer for the tax period (the value of the line indicator “Total for the year” in column 4 of Section I of the Income and Expense Accounting Book).

2.8. Line code 020 indicates the amount of expenses incurred by the taxpayer for the tax period (the value of the line indicator “Total for the year” in column 5 of Section I of the Income and Expense Accounting Book).

2.9. Line code 030 indicates the amount of the difference between the amount of the minimum tax paid for the previous tax period and the amount of tax calculated for the same period of time in the general procedure.

2.10. Line code 040 reflects the tax base for the tax period (line code 010 - line code 020 - line code 030).

A negative value for line code 040 is not reflected.

2.11. Line code 041 indicates the amount of losses received by the taxpayer for the tax period (line code 020 + line code 030 - line code 010).

A negative value for line code 041 is not reflected.

III. The procedure for filling out section II "Calculation of expenses

for the acquisition (construction, production) of fixed assets

and for acquisition (creation by the taxpayer himself)

intangible assets taken into account when calculating

tax base for the tax for the reporting (tax) period"

3.1. This section is filled out by a taxpayer who has chosen “income reduced by expenses” as the object of taxation.

3.2. When filling out this section, the taxpayer indicates the reporting (tax) period for which the calculation of expenses for the acquisition (construction, production, creation by the taxpayer himself) of fixed assets and intangible assets taken into account when calculating the tax base for the tax is made (I quarter, half a year, 9 months, year).

3.3. Expenses for the acquisition, construction and production of fixed assets, as well as for the completion, retrofitting, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition of intangible assets, the creation of intangible assets by the taxpayer himself, provided for in subparagraphs 1 and 2 of paragraph 1 of Article 346.16 of the Code , are determined in the manner established by paragraphs 3 and 4 of Article 346.16, subparagraph 4 of paragraph 2 of Article 346.17, paragraphs 2.1 and 4 of Article 346.25 of the Code.

Expenses for the acquisition (construction, production) of fixed assets, completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition (creation by the taxpayer himself) of intangible assets, taken into account in the manner prescribed by paragraph 3 of Article 346.16 of the Code, are reflected in the last date of the reporting (tax) period in the amount of amounts paid. In this case, during the tax period, expenses are accepted for reporting periods in equal shares. These expenses are taken into account only for fixed assets and intangible assets used in carrying out business activities.

3.4. Expenses for the acquisition (construction, production) of fixed assets, completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition (creation by the taxpayer himself) of intangible assets are reflected in the section in a positional manner separately for each object.

3.5. Column 1 indicates the serial number of the operation.

3.6. Column 2 indicates the name of the fixed asset or intangible asset in accordance with the technical passport, inventory cards and other documents for the fixed asset or intangible asset.

3.7. Column 3 indicates the date, month and year of payment for the item of fixed assets or intangible assets on the basis of primary documents (payment orders, receipts for cash receipts, other documents confirming the fact of payment).

3.8. Column 4 indicates the date, month and year of submission of documents for state registration of fixed assets, the rights to which are subject to state registration in accordance with the legislation of the Russian Federation (with the exception of fixed assets put into operation before 01/31/1998).

3.9. Column 5 indicates the day, month, year of commissioning (acceptance for accounting) of the fixed asset or intangible asset.

3.10. Column 6 indicates the initial cost of the acquired (constructed, manufactured) item of fixed assets during the period of application of the simplified taxation system and the initial cost of the acquired (created by the taxpayer himself) item of intangible assets during the application of the simplified taxation system, which are determined in the manner established by regulatory legal acts on accounting.

The initial cost of an acquired (constructed, manufactured) fixed asset during the period of application of the simplified taxation system is reflected in column 6 in the reporting (tax) period in which one of the following events occurred most recently: commissioning of a fixed asset object; submission of documents for state registration of rights to an object of fixed assets, payment (completion of payment) of expenses for the acquisition (construction, production) of an object of fixed assets.

The initial cost of an acquired (created by the taxpayer himself) object of intangible assets during the period of application of the simplified taxation system is reflected in column 6 in the reporting (tax) period in which the most recent one of the following events occurred: acceptance of the object of intangible assets for accounting, payment ( completion of payment) expenses for the acquisition (creation by the taxpayer himself) of an object of intangible assets.

In accordance with paragraph 4 of Article 346.16 of the Code, expenses for the completion, retrofitting, reconstruction, modernization and technical re-equipment of fixed assets for the purposes of Chapter 26.2 of the Code are determined taking into account the provisions of paragraph 2 of Article 257 of the Code, which establish what applies to these expenses. Expenses for completion, additional equipment, reconstruction, modernization and technical re-equipment are reflected in column 6 in the reporting (tax) period in which one of the following events occurred most recently: commissioning of a fixed asset facility; submission of documents for state registration of rights to an object of fixed assets, payment (completion of payment) of expenses for the acquisition (construction, production) of an object of fixed assets.

3.11. Column 7 indicates the useful life of an item of fixed assets or intangible assets, determined in the manner prescribed by paragraph 3 of Article 346.16 of the Code.

For fixed assets and intangible assets acquired (constructed, manufactured, created by the taxpayer himself) and put into operation (accepted for accounting) during the period of application of the simplified taxation system, column 7 is not filled in.

3.12. Column 8 indicates:

the residual value of acquired (constructed, manufactured) fixed assets, as well as acquired (created by the taxpayer himself) intangible assets before the transition to a simplified taxation system, taken into account in accordance with subparagraph 3 of paragraph 3 of Article 346.16 of the Code;

expenses for completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets acquired before the transition to the simplified taxation system, taken into account in accordance with subparagraph 1 of paragraph 3 of Article 346.16 of the Code.

In accordance with paragraph 3 of Article 346.16 of the Code, if the taxpayer has switched to a simplified taxation system with the object of taxation in the form of income reduced by the amount of expenses from other taxation regimes, the cost of fixed assets and intangible assets is taken into account in accordance with paragraphs 2.1 and 4 of the article Code 346.25 order.

When switching to a simplified taxation system for an organization from the general taxation regime, column 8 on the date of such transition reflects the residual value of each acquired (constructed, manufactured) fixed asset and acquired (created by the organization itself) intangible asset that were paid before the transition to the simplified taxation system, in the form of the difference between the purchase price (construction, manufacturing, creation by the organization itself) and the amount of accrued depreciation in accordance with the requirements of Chapter 25 of the Code.

When transitioning to a simplified taxation system for an organization applying the taxation system for agricultural producers (single agricultural tax) in accordance with Chapter 26.1 of the Code, column 8 as of the date of the specified transition reflects the residual value of each acquired (constructed, manufactured) fixed asset and acquired (created by itself) organization) of an intangible asset, determined based on their residual value as of the date of transition to payment of the unified agricultural tax, reduced by the amount of expenses determined in the manner prescribed by subparagraph 2 of paragraph 4 of Article 346.5 of the Code for the period of application of Chapter 26.1 of the Code.

When transitioning to a simplified taxation system for an organization that applies a taxation system in the form of a single tax on imputed income for certain types of activities in accordance with Chapter 26.3 of the Code, column 8 as of the date of this transition reflects the residual value of each acquired (constructed, manufactured) fixed asset and acquired (created by the organization itself) of an intangible asset before the transition to a simplified taxation system in the form of the difference between the purchase price (construction, manufacture, creation by the organization itself) of a fixed asset and an intangible asset and the amount of depreciation accrued in the manner established by the legislation of the Russian Federation on accounting, for the period of application of the taxation system in the form of a single tax on imputed income for certain types of activities.

The residual value of each acquired (constructed, manufactured) fixed asset and acquired (created by the organization itself) intangible asset before the transition to the simplified taxation system is indicated in column 8 in the reporting (tax) period of application of the simplified taxation system in which the most recent one of the following events: commissioning of an object of fixed assets (acceptance of an object of intangible assets for accounting), submission of documents for state registration of rights to an object of fixed assets, payment (completion of payment) of expenses for the acquisition (construction, production, creation by the taxpayer himself) of an object of fixed assets and intangible assets.

Expenses for completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets acquired before the transition to the simplified taxation system are reflected in column 8 in the reporting (tax) period in which, during the period of application of the simplified taxation system, one of the following occurred most recently events: commissioning of fixed assets; submission of documents for state registration of rights to an object of fixed assets, payment (completion of payment) of expenses for the acquisition (construction, production) of an object of fixed assets.

Individual entrepreneurs, when transitioning from other taxation regimes to a simplified taxation system, have the right to apply the rules established for organizations when determining the residual value.

3.13. Column 9 indicates the number of quarters of operation in the tax period of the paid and put into operation (accepted for accounting) fixed assets or intangible assets.

3.14. Column 10 indicates the share of the cost of the acquired (constructed, manufactured, created by the taxpayer himself) fixed asset or intangible assets, accepted as expenses in accordance with paragraph 3 of Article 346.16 of the Code, for the tax period.

3.15. Column 11 indicates the share of the cost of the acquired (constructed, manufactured, created by the taxpayer himself) fixed asset or intangible asset, accepted as expenses in each quarter of the reporting (tax) period, determined as the ratio of the data in column 10 to the data in column 9.

The value of this indicator is rounded to the second decimal place.

3.16. Column 12 reflects the amount of expenses for the acquisition (construction, production) of fixed assets, completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition (creation by the taxpayer himself) of intangible assets, included in the expenses taken into account when calculating tax base for the tax for each quarter of the tax period.

Moreover, for fixed assets or intangible assets acquired (constructed, manufactured, created by the taxpayer himself) and put into operation (accepted for accounting) during the period of application of the simplified taxation system, this amount is determined as the product of columns 6 and 11, divided by 100 .

For fixed assets and intangible assets acquired (constructed, manufactured, created by the taxpayer himself) before the transition to the simplified taxation system, this amount is determined as the product of columns 8 and 11, divided by 100.

The amount of expenses related to each quarter of the tax period in this column is reflected on the last day of the reporting (tax) period in column 5 of section I of the Income and Expense Accounting Book.

3.17. Column 13 reflects the amount of expenses for the acquisition (construction, production) of fixed assets, completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition (creation by the taxpayer himself) of intangible assets, included in the expenses taken into account when calculating tax base for the tax period. This amount of expenses is determined as the product of columns 12 and 9.

3.18. Column 14 reflects the amount of expenses for the acquisition (construction, production) of fixed assets, completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets, as well as expenses for the acquisition (creation by the taxpayer himself) of intangible assets, taken into account as expenses when calculating the tax tax bases for previous tax periods (data from column 13 of this section for previous tax periods).

For fixed assets and intangible assets acquired (constructed, manufactured, created by the taxpayer himself) and put into operation (accepted for accounting) during the period of application of the simplified taxation system, column 14 is not filled in.

3.19. Column 15 reflects the remaining costs for the acquisition (construction, production, creation by the taxpayer himself) of fixed assets and intangible assets, subject to write-off in subsequent tax periods (column 8 - column 13 - column 14).

For fixed assets and intangible assets acquired (constructed, manufactured, created by the taxpayer himself) and put into operation (accepted for accounting) during the period of application of the simplified taxation system, column 15 is not filled in.

3.20. Column 16 indicates the date, month and year of disposal (sale) of the fixed asset or intangible asset.

3.21. The final line of this section for the reporting (tax) period reflects the sum of the values of indicators in columns 6, 8, 12 - 15.

IV. The procedure for filling out Section III "Calculation of the amount of loss,

reducing the tax base for the tax paid

due to the use of a simplified taxation system

for the tax period" (line codes 010 - 250)

4.1. This section is filled out by a taxpayer who has chosen the object of taxation in the form of income reduced by the amount of expenses, and who, based on the results of the previous tax period(s), received losses from business activities in respect of which the simplified taxation system is applied.

The taxpayer has the right to carry forward a loss to future tax periods within 10 years following the tax period in which the loss was incurred. The taxpayer has the right to transfer to the current tax period the amount of loss received in the previous tax period. A loss not carried forward to the next year may be carried forward in whole or in part to any year out of the next nine years. If a taxpayer received losses in more than one tax period, such losses are carried forward to future tax periods in the order in which they were received.

4.2. Line code 010 indicates the amount of losses received based on the results of previous tax periods that were not carried forward to the beginning of the expired tax period, and line codes 020 - 110 indicate the amount of losses by year of their formation (corresponding to the values of indicators for line codes 150 - 250 of section III Books of accounting of income and expenses for the previous tax period).

4.3. Line code 120 indicates the tax base for the expired tax period (corresponds to the value of the indicator in line code 040 of the reference part of Section I of the Book of Income and Expenses).

4.4. Line code 130 indicates the amount of losses by which the taxpayer actually reduced the tax base for the expired tax period (within the amount of losses received based on the results of previous tax periods that were not carried forward to the beginning of the expired tax period, indicated on page 010).

4.5. Line code 140 indicates the amount of loss for the expired tax period (corresponds to the value of the indicator in line code 041 of the reference part of Section I of the Book of Income and Expenses).

4.6. Line code 150 indicates the amount of losses at the beginning of the next tax period, which the taxpayer has the right to transfer to future tax periods (corresponds to the value of the indicator for line code 010 - line code 130 + line code 140).

The value of the indicator by line code 150 is transferred to section III of the Book of Income and Expenses for the next tax period and is indicated by line code 010.

4.7. Line codes 160 - 250 indicate the amounts of losses that were not transferred when the tax base was reduced for the past tax period, by the year of their formation. The sum of the indicator values for line codes 160 - 250 corresponds to the indicator value for line code 150 of Section III of the Book of Income and Expenses.

The values of indicators for line codes 160 - 250 are transferred to section III of the Book of Income and Expenses for the next tax period and are indicated by line codes 020 - 110.

V. The procedure for filling out section IV "Costs,

provided for in paragraph 3.1 of Article 346.21 of the Tax Code

Code of the Russian Federation, reducing the amount of tax,

paid in connection with the application of the simplified system

taxation (advance tax payments)

for the reporting (tax) period"

5.1. This section is filled out by the taxpayer who has chosen “income” as the object of taxation.

5.2. This section reflects insurance premiums, temporary disability benefits paid to employees and payments (contributions) under voluntary personal insurance contracts provided for in paragraph 3.1 of Article 346.21 of the Code, which reduce the amount of tax paid in connection with the use of the simplified taxation system (advance tax payments).

5.3. Column 1 indicates the serial number of the transaction being registered.

5.4. Column 2 indicates the date and number of the primary document on the basis of which the registered transaction was carried out.

5.5. Column 3 indicates the period for which insurance premiums were paid and temporary disability benefits provided for in columns 4 - 9 were made.

5.6. Column 4 reflects insurance contributions for compulsory pension insurance.

ConsultantPlus: note.

From January 1, 2013, individual entrepreneurs who do not make payments or other remuneration to individuals pay insurance contributions to the Pension Fund and the Compulsory Medical Insurance Fund in a fixed amount, and not based on the cost of the insurance year, as was previously the case. On the amount of insurance premiums paid by this category of payers from January 1, 2017, see Article 430 of the Tax Code of the Russian Federation.

5.7. Column 5 reflects insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity.

5.8. Column 6 reflects insurance premiums for compulsory health insurance.

Paragraphs two and three are no longer valid as of January 1, 2018. - Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n.

5.9. Column 7 reflects insurance contributions for compulsory social insurance against industrial accidents and occupational diseases.

5.10. Column 8 reflects the costs of paying temporary disability benefits in accordance with the legislation of the Russian Federation (with the exception of industrial accidents and occupational diseases) for days of temporary disability of the employee, which are paid at the expense of the employer and the number of which is established by the Federal Law of December 29, 2006 year N 255-FZ "On compulsory social insurance in case of temporary disability and in connection with maternity", in the part not covered by insurance payments made to employees by insurance organizations that have licenses issued in accordance with the legislation of the Russian Federation to carry out the corresponding type of activity , under agreements with employers in favor of employees in the event of their temporary disability (except for industrial accidents and occupational diseases) for days of temporary disability, which are paid at the expense of the employer and the number of which is established by Federal Law of December 29, 2006 N 255-FZ "On compulsory social insurance in case of temporary disability and in connection with maternity."

5.11. In column 9, payments (contributions) under voluntary personal insurance contracts concluded with insurance organizations that have licenses issued in accordance with the legislation of the Russian Federation to carry out the relevant type of activity, in favor of employees in the event of their temporary disability (except for industrial accidents and occupational diseases) for days of temporary disability, which are paid at the expense of the employer and the number of which is established by Federal Law of December 29, 2006 N 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity.” The specified payments (contributions) reduce the amount of tax (advance tax payments) if the amount of insurance payment under such contracts does not exceed the amount of temporary disability benefits determined in accordance with the legislation of the Russian Federation (except for industrial accidents and occupational diseases) for days of temporary employee disability, which is paid at the expense of the employer and the number of which is established by Federal Law of December 29, 2006 N 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity.”

5.12. Column 10 reflects the total amount of insurance premiums paid to employees of temporary disability benefits and payments (contributions) under voluntary personal insurance contracts for the reporting (tax) period (corresponds to the sum of the values of the total line indicators for the reporting (tax) period in columns 4 - 9) .

VI. The procedure for filling out section V "Amount

trade tax, which reduces the amount of tax paid

due to the use of a simplified taxation system

(advance tax payments) calculated for the object

taxation depending on the type of business activity,

in respect of which a trade tax has been established,

for the reporting (tax) period"

(introduced by Order of the Ministry of Finance of Russia dated December 7, 2016 N 227n)

6.1. This Section is filled out by a taxpayer who has chosen “income” as the object of taxation.

6.2. This section reflects the amount of the paid trade fee, which reduces the amount of tax paid in connection with the application of the simplified taxation system (advance tax payments), calculated for the object of taxation from the type of business activity in respect of which a trade fee is established in accordance with Chapter 33 of the Code.

6.3. Column 1 indicates the serial number of the transaction being registered.

6.4. Column 2 indicates the date and number of the primary document on the basis of which the registered transaction was carried out.

6.5. Column 3 indicates the period for which the trade fee was paid.

6.6. Column 4 indicates the amount of the trade fee paid.

KUDiR USN patent (PSN)

COMPLETING THE INDIVIDUAL INCOME ACCOUNTING BOOK

ENTREPRENEURSHIP USING PATENTS

TAX SYSTEM

I. General requirements

1.1. Individual entrepreneurs applying the patent taxation system (hereinafter referred to as taxpayers) maintain the Income Book of individual entrepreneurs applying the patent taxation system (hereinafter referred to as the Income Accounting Book), in which, in chronological order, based on primary documents, they reflect in a positional way all business transactions related to receipt of income from sales in the tax period (the period for which the patent was received).

1.2. Taxpayers must ensure the completeness, continuity and reliability of accounting for income from sales received in connection with the implementation of types of business activities, taxation of which is carried out under the patent taxation system.

1.3. The Income Book is maintained in Russian. Primary accounting documents compiled in a foreign language or languages of the peoples of the Russian Federation must have a line-by-line translation into Russian.

1.4. The income accounting book can be kept both on paper and in electronic form. When maintaining the Income Book in electronic form, taxpayers are required to print it out on paper at the end of the tax period. For each tax period, a new Income Accounting Book is opened.

1.5. The income ledger must be laced and numbered. On the last page of the Income Accounting Book, numbered and laced by the taxpayer, the number of pages it contains is indicated, which is confirmed by the taxpayer’s signature and sealed with the taxpayer’s seal (if any).

On the last page, numbered and laced by the taxpayer of the Income Book, which was kept electronically and printed on paper at the end of the tax period, the number of pages it contains is indicated, which is confirmed by the taxpayer’s signature and sealed with the taxpayer’s seal (if any).

1.6. Correction of errors in the Income Book must be justified and confirmed by the taxpayer’s signature, indicating the date of correction and the taxpayer’s stamp (if any).

II. Procedure for filling out Section I "Income"

2.1. Column 1 indicates the serial number of the transaction being registered.

2.2. Column 2 indicates the date and number of the primary document on the basis of which the registered transaction was carried out.

2.3. Column 3 indicates the content of the registered transaction.

2.4. Column 4 reflects income from sales received in connection with the implementation of business activities specified in the patent, and determined in accordance with Article 249 of the Code. The procedure for determining, recognizing and accounting for income from sales under the patent taxation system is established by paragraphs 2 - 5 of Article 346.53 of the Code.

Column 4 does not take into account income received from other types of business activities, the taxation of which is carried out in accordance with other taxation regimes.

KUDIR on OSNO

Organizations on OSNO do not maintain KUDIR

Entrepreneurs submit 3-personal income tax on OSN and keep a special book: KUDIR IP on OSNO for personal income tax.

This book is very different from the one in the simplified version.

Unified agricultural tax

Accounting for income and expenses under the Unified Agricultural Tax is carried out using the cash method. Tax accounting for the purposes of calculating the Unified Agricultural Tax for organizations is carried out on the basis of accounting data (i.e., a balance sheet and profit and loss account are needed). For individual entrepreneurs - in the book of income and expenses of individual entrepreneurs using the Unified Agricultural Tax.

UTII

KUDIR is not recorded on UTII. There is no special book form for UTII. Sometimes, for separate accounting (when applying other tax regimes), it is still necessary to keep records of income under UTII. Then you can take a sample book for the simplified tax system.

The income book for individual entrepreneurs on the simplified tax system is a mandatory type of reporting for an individual entrepreneur and it is by it that his activities are monitored. It has a standardized form approved by the Ministry of Finance of the Russian Federation. The rules for filling it out are strictly regulated by Russian legislation. In this book, records of commercial activities are kept, and then, based on its data, taxes are calculated. Therefore, the tax office tries to control the correct filling out of the accounting book.

Today we will look at how this book of accounting for individual entrepreneurs using the simplified tax system with “Income” in 2017 should be filled out. We’ll tell you what to consider when filling out forms, and not to pay special attention. The article will provide examples of filling out book forms. Filling out the book yourself if you follow our recommendations is not at all difficult; today we will tell you in detail how to do this.

Separately, in our article we will consider the innovations of 2017. We will tell you in detail what has already changed in 2017 and what else is planned to change in the very near future.

Rules for maintaining a book of income and expenses

KUDIR- a book of accounting for business transactions, which is required to be maintained by individual entrepreneurs working on the simplified tax system.

Let's consider maintaining a book of accounting for individual entrepreneurs working for the National Tax Service with income taxation at a 6% tax rate.

All individual entrepreneurs using the simplified tax system must maintain their own KUDIR.

KUDIR- this is a type of reporting for an individual entrepreneur and it must be filled out regularly. Let us note that the tax inspector has the right to demand it and the entrepreneur is obliged to provide his KUDIR upon the first request. In case of failure to provide correctly completed reports, a fine may be imposed, as for any other reports not submitted in a timely manner.

If, at the first request of the tax inspector, the entrepreneur was unable to provide KUDIR, he may be fined 200 rubles (see Article 126 of the Tax Code). If the accounting book is not found during an on-site inspection, the fine may already be 10,000 rubles (see Article 120 of the Tax Code). If the individual entrepreneur was unable to provide accounting books for more than one year, then the fine would be 30 thousand rubles. If the tax authorities can prove that the lack of accounting for business activities led to an underestimation of taxes, then the individual entrepreneur faces a fine of at least 40 thousand rubles.

However, we note that the requirement to present KUDIR must be formalized in writing by an employee of the Federal Tax Service and can be presented during an on-site tax audit or in a number of other cases.

KUDIR refers to tax registers, which are the basis for the assessment of taxes, and therefore, its absence is tantamount to a violation of the rules for keeping records of income and expenses.

Now, as before, it is not necessary to submit the KUDIR for regular inspection to the Federal Tax Service.

Its form is the same for all individual entrepreneurs, but for different tax regimes the methods of maintaining it are slightly different.

KUDIR can be kept in the old way - on paper, making notes by hand, you can keep an electronic version on a computer and, if necessary, print it out. Now there are online services for maintaining KUDIR.

You can choose any of the options for keeping records, the main thing is to keep it correctly and be able to print it out, number it, sew it at the right time and present it to the tax authorities.

KUDIR has an annual reporting form, i.e. For every new year, a new book is started. In this case, the book for the past reporting period is printed, numbered, stitched, certified with the seal of the individual entrepreneur (if any) and his signature. This book is subject to mandatory storage and the tax office has the right to conduct an audit for the last three years.

If the individual entrepreneur did not conduct commercial activities in the past year, then a “zero” book must be printed and stapled. If there were unfilled sections of the book, they are also numbered and filed.

KUDIR is an annual reporting form for individual entrepreneurs. It is worth remembering this and understanding that the same requirements apply to it as any other reporting. It is standardized and has a shelf life of 4 years.

If an individual entrepreneur has small annual turnover, then the accounting book can be kept on paper, making entries by hand.

If the turnover is large, then it is better to keep records using specialized services. It’s possible that you can simply run it on your computer in Excel.

In the accounting book, each transaction is recorded in chronological order on a separate line, and it must have documentary evidence. The supporting documents usually include: invoices, payment orders, checks, contracts, etc.

Basic general rules for maintaining KUDIR for individual entrepreneurs on the simplified tax system for “Income”:

- KUDIR is an annual reporting form and therefore every year an entrepreneur must open a new accounting book, for a new calendar year - a new tax period

- Entries in the book must be made line by line, i.e. one line - one operation

- records are kept in chronological order

- records are kept only in full rubles

- at the end of the reporting tax period, in this case the calendar year, KUDIR must be printed

- sections of the book that are not completed are still printed

- if the individual entrepreneur did not conduct any commercial activity during this year, he prints out a “zero book”

- at the end of the annual tax period, the accounting book is numbered and stitched, certified by the signature of the individual entrepreneur; if there is a seal, it is also certified by a seal

- The accounting book must be kept for 4 years

- replenishment of a current account is not income from business activities, and such transactions are not recorded in the ledger

- The KUDIR form is a unified reporting form, its forms were approved by Order of the Ministry of Finance No. 135n on October 22, 2012.

The standardized KUDIR form contains:

- Title page on which the individual entrepreneur’s taxpayer data is written

- Section 1 “Income and Expenses”, it is filled out by all individual entrepreneurs

- Section 2 “Expenses for fixed assets and intangible assets” - individual entrepreneur on the simplified “Income” system is not filled out

- Section 3 Calculation of loss amounts - IP on the simplified tax system “Income” is not filled out

- Section 4 Insurance premiums - to be completed by all individual entrepreneurs.

We have outlined the basic rules for maintaining KUDIR and the requirements for it. Next, we will analyze all sections of the accounting book in more detail and the rules for filling it out.

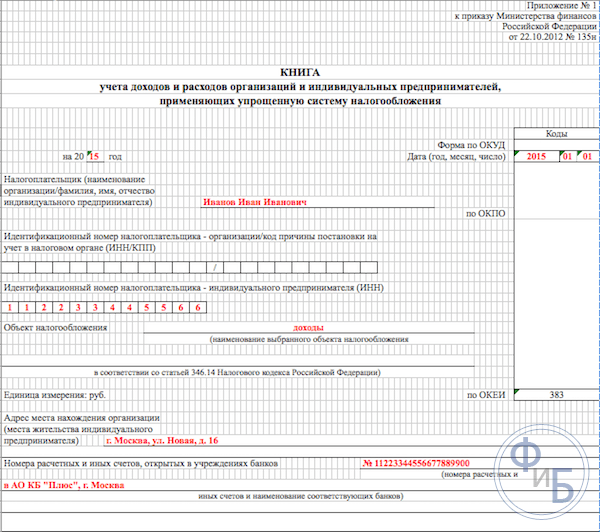

Filling out the accounting book begins with the design of the title page:

- the column “OKUD form” is not filled out

- in the “Date” column, enter the date of opening of the book - the date of its first entry

- fill in the field for what period the book is open - for 2017

- OKPO field indicates the code from statistics

- The full name of the individual entrepreneur is entered in the “Taxpayer” column

- In the INN/KPP column we indicate the corresponding individual entrepreneur numbers

- in the column “Object of taxation” - write “Income”

- In the address line we indicate the individual’s residential address

- further at the bottom of the page, fill in the bank details fields - indicate the details of the individual entrepreneur’s current account.

In section 1 of the accounting book, individual entrepreneurs who are under the income tax regime record their income. The form is designed to be completed quarterly and contains 4 tables. Each operation is recorded on a separate line; you can add more lines if necessary. The tables have five vertical columns that need to be filled out, as follows:

- transaction numbers, transactions are in chronological order

- date and number of the document that forms the basis of the transaction; dates of invoices, bills, etc. are indicated here.

- content of the operation - it is necessary to briefly reflect its essence

- in the income column - write down the amount of income received

- the expenses column - for individual entrepreneurs with taxation of only income, is not filled in.

And so, section 1 is filled out sequentially throughout the year.

Let us only note that, for example, cash revenue is summed up for the day and reflected in one entry; the basis of the operation is the Z-report. Thus, we enter the date and number of this cash report into the table. You can do the same with other similar income. When a stream of payments arrives in your current account, you can rely on the daily bank statement.

Note that sometimes there are cases when it is necessary to make a chargeback, then an entry is made in the book in the income column, as usual, but with a minus.

After the completion of each quarter, the section summarizes the total numerical results in the corresponding rows of the tables. In specially designated lines, cumulative cumulative totals for six and nine months are reflected, and the annual total is calculated.

In the expenses column, entries for this taxation system are made extremely rarely, for example, if expenses were incurred using funds received under the SME support program from government subsidies. These amounts must be reflected in both income and expense columns so that they do not contribute to the tax base.

Note that there are other non-taxable incomes; they do not need to be recorded in KUDIR. Often individual entrepreneurs receive income from sales and income “outside sales”; these concepts must be separated.

Completing Section 2 “Calculation of costs for the acquisition of fixed assets and intangible assets”

Completing Section 3 “Calculation of the amount of loss that reduces the tax base”

This section, individual entrepreneurs on the simplified tax system only for income, is not filled out. It is intended for individual entrepreneurs who also keep track of expenses. Therefore, in the printout of the accounting book for the reporting period, this section will be filed blank.

Completing Section 4 “Expenses that reduce the amount of tax”

In section 4, it is necessary to record the amounts of contributions paid quarterly and in the corresponding lines the data is given in cumulative totals for six and nine months, and the annual total is calculated. The columns of the table indicate each of the insurance premiums that must be specified. Contributions are also indicated for employees if they were hired by an individual entrepreneur during this period. Further, advance payments of taxes must be taken into account when calculating the taxable base within the established limits.

If an individual entrepreneur has hired workers, then the following payments must be indicated in the section:

- contributions made from employee salaries

- payments for sick leave paid from the individual entrepreneur’s own funds

- voluntary insurance payments

- fixed amounts of insurance premiums that were paid by the individual entrepreneur for himself

In 2016, the following innovations appeared for individual entrepreneurs using the simplified tax system under the “income” taxation system:

- The procedure for filling out Section 4 was clarified, regarding the recording of a fixed amount of insurance premiums.

- KUDIR was supplemented with a new section 5 “Amounts of trade tax”, which will reflect the amount of paid trade tax.

- A new legislative provision has appeared stating that income received by an individual entrepreneur from foreign organizations controlled by him is not recorded in the KUDIR of section 1, column 4. Taxation of such income is carried out separately.

Now let's talk about this in more detail.

It should be noted here that from 2017 Art. 430 of the Tax Code on fixed insurance premiums. That is, at the legislative level, there was a unification of the amounts of insurance premiums for the minimum wage and contributions of 1% on incomes of more than 300 thousand rubles. These new rules apply to individual entrepreneurs who work without hiring employees and are on the simplified tax system based on “income” and pay only their insurance premiums.

This means that now these individual entrepreneurs will record in the accounting book all their deductions for compulsory insurance: both from the minimum wage and 1% from incomes over 300 thousand rubles in a fixed amount. Previously, until 2017, tax inspectors often refused to reduce the amount of 6% tax due to “1% contributions”. Accordingly, questions often arose when filling out KUDIR.

The emerging norm of legislation on controlled foreign organizations is designed to clearly distinguish at the legislative level between taxation systems for individual entrepreneurs when paying a single tax on a simplified system and the application of income tax rates. Thus, now the Tax Code (see Article 248) clearly states that income from foreign individual entrepreneurs does not fall under the simplified tax system. Income tax must be paid on such income.

At the end of 2016, the KUDIR form was revised - a new fifth section was included in it. However, the new form of the book will begin to be used only in 2018, and accounting in the coming 2017 will continue to be carried out according to the accounting books of the previous model.

A new section of the book concerns accounting for trade fees, which will reduce the amount of single tax paid. Please note that the trade tax is currently only valid in Moscow. The new section will be filled in similarly to other sections of the book, i.e. in chronological order, indicating the details of documents - the basis of business transactions.

Conclusion

The accounting book is the main form of reporting for an individual entrepreneur; it reflects transactions related to the implementation of his commercial activities. The form of the book is standardized, the rules for filling it out are prescribed by law. When conducting it, you must adhere to all applicable legal provisions.

The Tax Inspectorate supervises the payment of taxes on the commercial activities of entrepreneurs, namely through control over the keeping of records of commercial transactions. For non-compliance with the rules for maintaining KUDIR, the law provides for the imposition of fines on entrepreneurs.

The article examined in detail the filling out of sections of the accounting book, provided samples of standard forms and examples of how to fill them out.

Separately, in the article we touched upon the latest legislative innovations related to the management of KUDIR in 2017. They talked about the prepared new form of the accounting book.

When keeping records, it is better to adhere to the above recommendations and then there will be fewer questions from the tax inspectorate and paperwork. Filling out the accounting book yourself is not at all difficult; you can also use specialized online accounting services.

The ledger for accounting income and expenses is a special register where taxpayers using the simplified taxation system (STS) enter business transactions for subsequent calculation of the tax base for the STS tax.

The obligation to keep a book of income and expenses, or KUDiR, as accountants often call it, is established by Article 346.24 of the Tax Code of the Russian Federation.

If KUDiR is not maintained or there are violations in filling it out, you can earn a fine from 10,000 to 30,000 rubles. And if violations lead to an underestimation of the tax base, a fine of 20% of the amount of unpaid tax. This is enshrined in Article 120 of the Tax Code of the Russian Federation.

At the same time, there is no obligation to submit KUDiR to the tax office. If the tax authorities require you to provide a Book of Income and Expenses during an audit, then you are required to provide the Book in paper form, bound, numbered and signed.

KUDiR may be needed in order to show the expenditure of targeted financing, or to show the Pension Fund of Russia income to determine the rate of insurance premiums for individual entrepreneurs, or in a bank for a loan.

The book is started for a year. It can be maintained in paper and electronic form. Of course, many accounting programs and web services (such as Kontur.Accounting or Elba) allow you to maintain a book in electronic form with varying degrees of simplicity. If the tax office requires it, you can print it out and take it.

How to fill out the Income and Expense Accounting Book (KUDiR)

We look forward to your feedback. Fill out KUDiR correctly;)

Try working in Kontur.Accounting - a convenient online service for maintaining accounting and sending reports via the Internet.

The book of accounting for income and expenses (abbreviated as KUDiR) in 1C 8.3 is maintained by organizations and entrepreneurs that use the simplified taxation system (STS).

Let's start with a simple question: where can I find KUDiR in 1C? It can be found as follows: go to the “Reports” menu, then in the “STS Reports” section, click on the “STS Book of Income and Expenses” link. We get to the book filling window:

The book is filled out automatically, quarterly. Usually it is formed at the end of the year and submitted to the tax inspector along with regulated accounting reports.

The book of income and expenses contains several sections:

- income and expenses are indicated quarterly, from the beginning of the year to the end of the year;

- expenses for fixed assets and intangible assets;

- section with calculation of damages;

- and a section where you can indicate amounts that reduce taxation for one reason or another.

Basically, the book is formed according to documents for the sale of goods, services and according to documents for the receipt of goods and services.

Important to consider that sales (expenses) will be included in the book of income and expenses after payment for goods or services (however, you need to make the appropriate settings in the program for this; I have highlighted it in the figure). Even before creating a book, you need to carry out the necessary regulatory operations, which are carried out at the end of the quarter. For example, close the month.

Get 267 video lessons on 1C for free:

Setting up the formation of a ledger for accounting income and expenses in 1C 8.3

Before forming KUDIR, you should check. They can affect the correct formation of the book.

Let's go to the "Main" menu, then follow the "Organizations" link to the list of organizations. Let’s go to the organization we need, and then to “Accounting Policies”. In 1C, 90% of cases like “KUDiR is not filled in” or “does not fall into KUDiR” are resolved by setting up accounting policies.

Click on the “Recognition of expenses” button (this button appears when the object of taxation is “income - expenses”).

In addition to the general settings in the Accounting Policy, there are also settings for printing the book itself.

Let's return to KUDIR and click the "Show settings" button.

A window with settings will open:

The most interesting and necessary thing here is the “Output transcripts” checkbox. By checking this box, you can see which document generated this or that income or expense.

Other settings affect the appearance of the book. Different tax authorities require it differently.

Adjusting entries in the income and expense ledger in 1C Accounting 8.3

As I already mentioned, the book is generated automatically. But sometimes it is necessary to manually adjust the data for tax accounting. For this purpose, the document “Records of the book of income and expenses (STS)” is used.

Dream Interpretation: Why do you dream about Legs?

Dream Interpretation: Why do you dream about Legs? Order of the Ministry of Finance on the forms of financial statements of organizations

Order of the Ministry of Finance on the forms of financial statements of organizations What is the procedure for preparing cash documents?

What is the procedure for preparing cash documents?